What the world doesn't get about alternative investments

Plus: a flow chart!

August 28, 2025

There have been a lot of headlines recently about financial companies giving individual customers access to alternative investments like private equity (taking stakes in private companies) and private credit (loans to companies made outside of the banking system). Some of the coverage is positive, and some takes a more skeptical approach. As a place that’s offered alternatives since 2021, we continue to believe it is in investors’ best interests to make private-market investing more public. (If you’re wondering if alts are right for you, we put together a flow chart at the bottom of this newsletter to help you figure that out!)

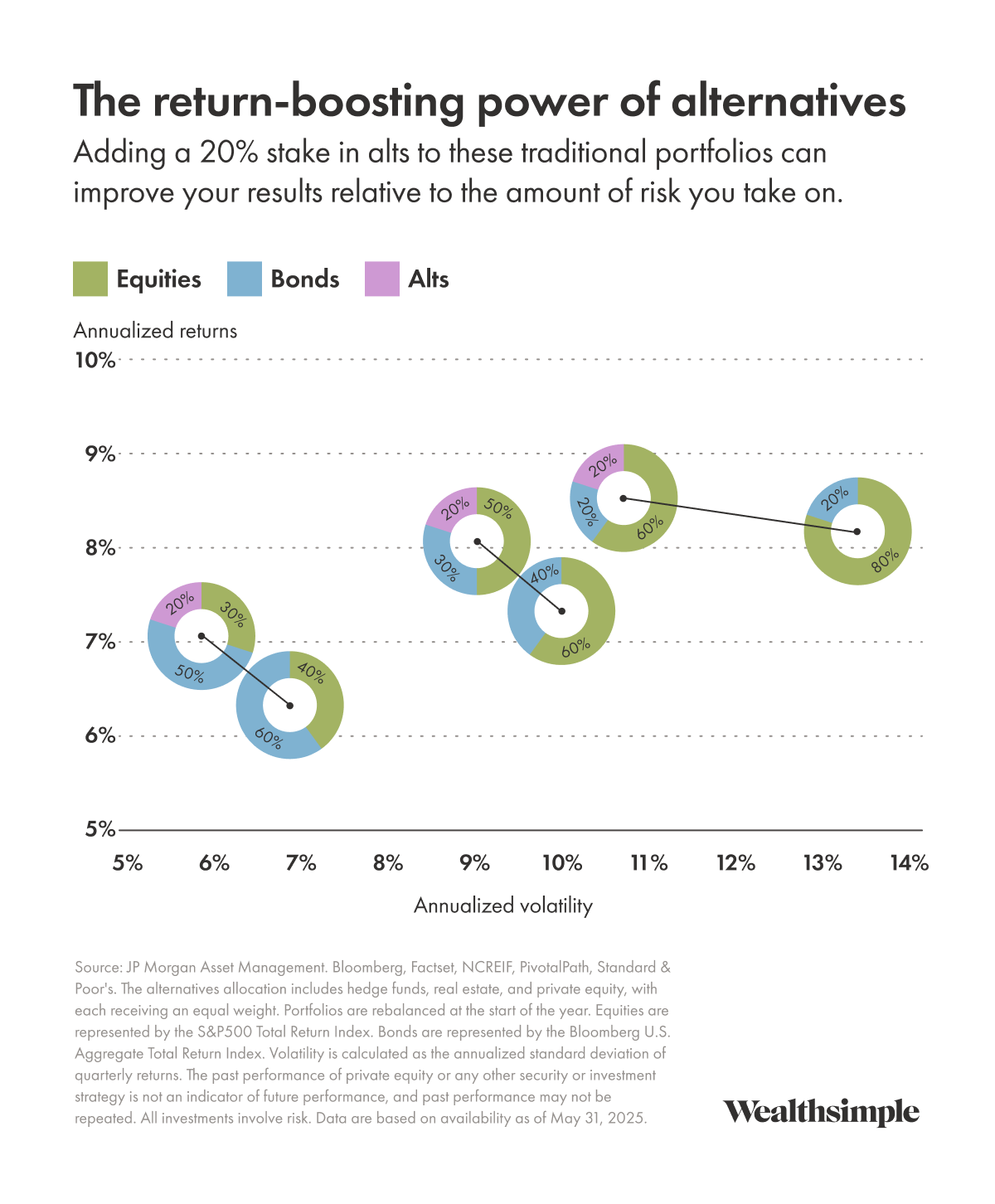

Why? For investors with a long-enough time horizon and a strong financial foundation, alternatives can provide access to differentiated sources of return and risk that traditional public-market portfolios lack, like the illiquidity premium. In fact, adding alternative investments to portfolios can improve expected annualized returns while reducing annualized volatility (at least, perceived volatility). The potential improvements to the return-to-risk ratio is why so many institutional investors use alternatives in their portfolio. If you’re working in education, for the government, or even just expecting to collect CPP at some point, you’ve likely benefited from exposure to alternatives already through your pension.

Here’s a look at what alts can do when added to various portfolios:

Of course, we also realize that some potential investors have concerns about the asset class. To them, alternatives sound too good to be true or too expensive to be worth it. Those are valid concerns, but we think they’re based on misconceptions. Which is why we’re dedicating this month’s newsletter to the five most common issues people raise, along with our perspective on each. If you have any questions we didn’t address, drop them in the feedback form at the end of this email and we’ll do our best to get back to you.

Big concern #1: Alternatives are only a good fit for super wealthy people and institutions

Historically, alternative investments required high minimums, offered limited liquidity, lacked transparency, and could involve waiting years to see your money actually invested — all things that the average retail investor couldn’t handle. But that’s no longer the case, since brokerages are now able to pool investments to lower the individual minimums, and since recent innovations like evergreen funds offer rolling investment and exit opportunities, as opposed to having small, set windows for both.

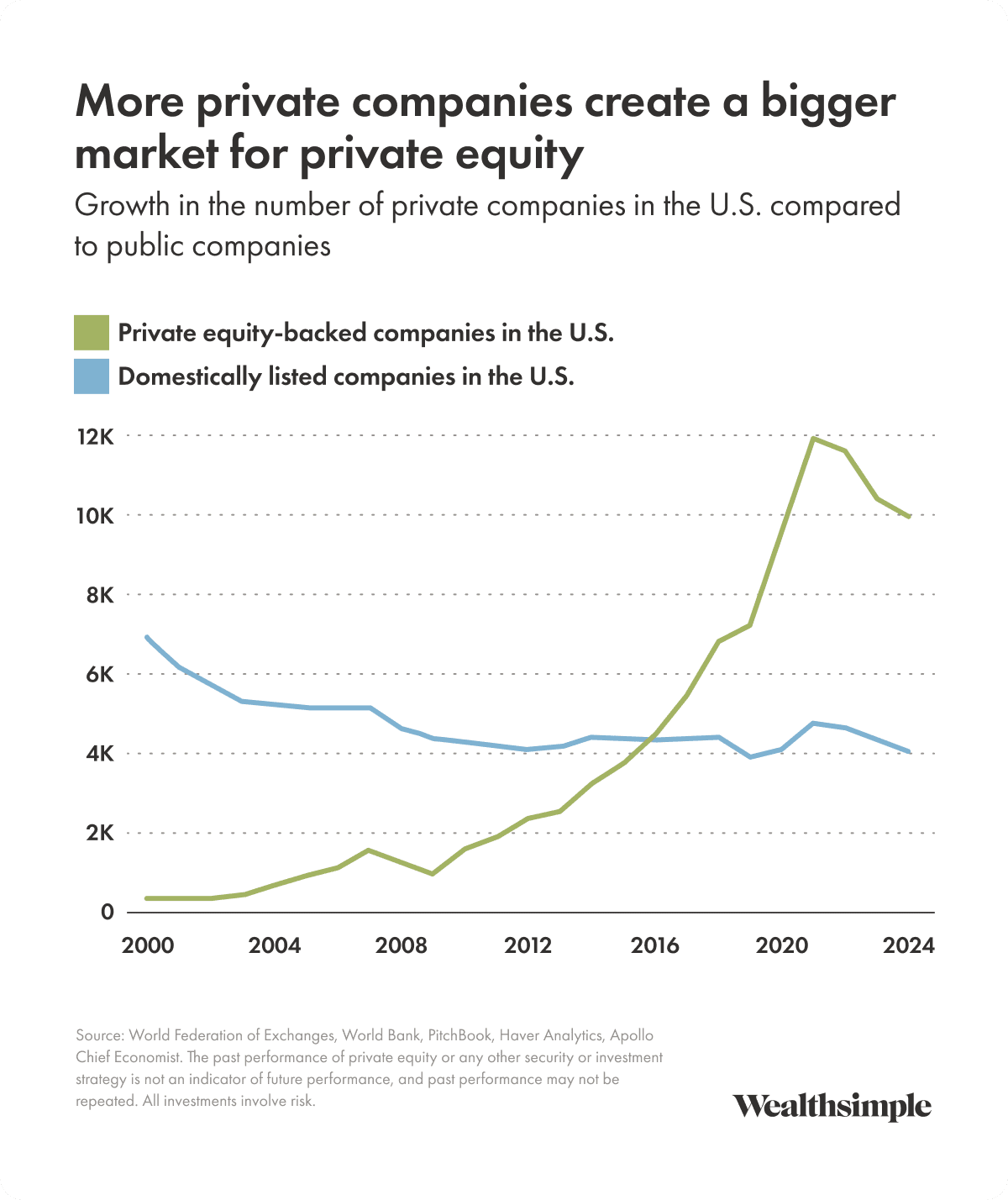

Big concern #2: There aren’t enough good investment opportunities for all of these new private-market investors

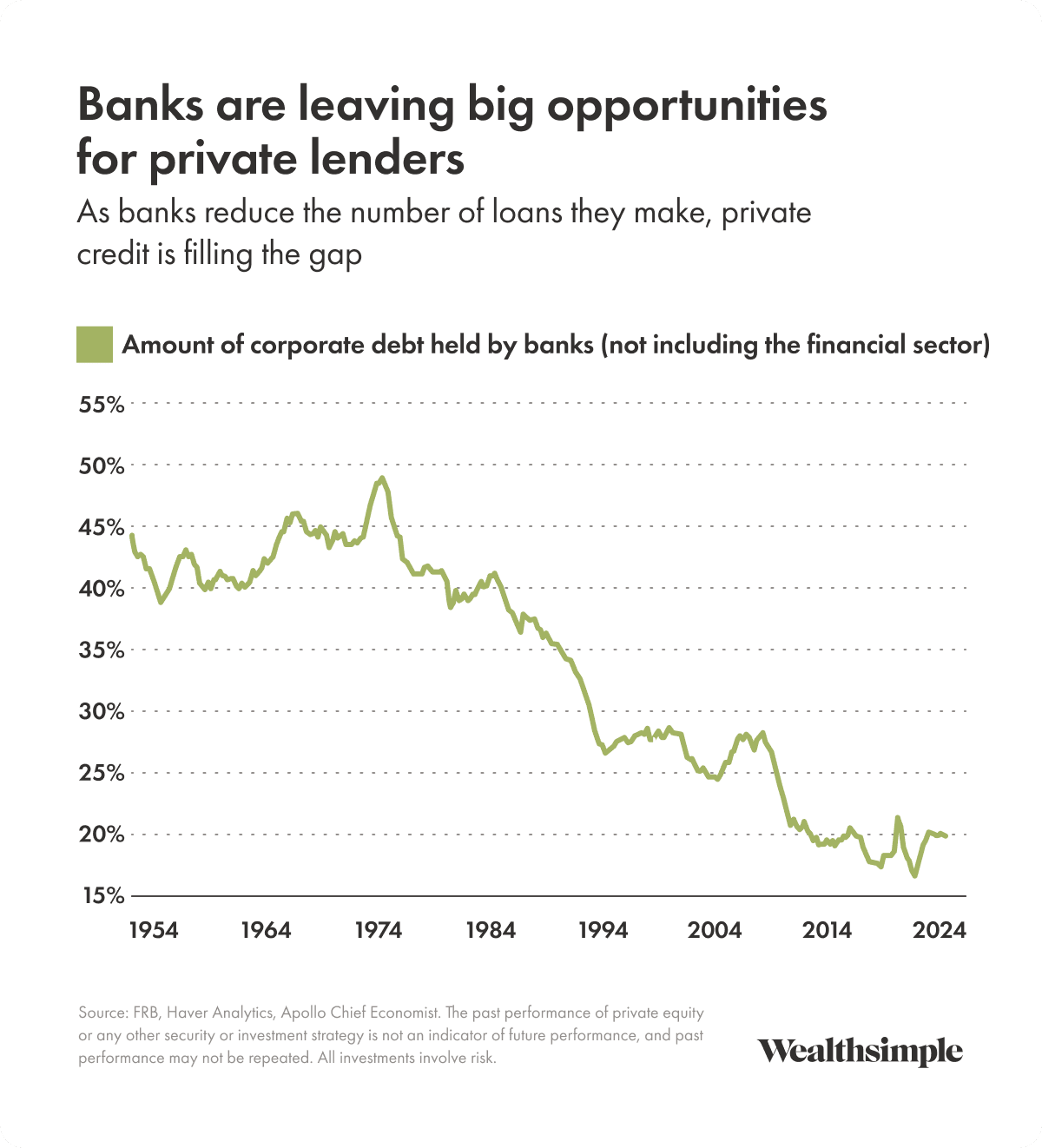

It’s true that the amount of money in private markets has grown rapidly in recent years. But there has also been a major surge in the need for this type of financing, as many companies are choosing to remain private to be able to build their businesses without facing the short-term pressure – and scrutiny – of delivering quarterly earnings growth that comes with going public. (See the chart below.) Plus, in the credit world, banks have tightened their lending practices in response to heightened regulatory standards and higher capital requirements introduced after the 2008 financial crisis, as you can see in the following chart. Private markets have had to step in to fill that void.

Recent data shows there are approximately 140,000 private companies globally with annual revenues over $100 million, compared to just 19,000 public companies of similar size. That means private companies outnumber public ones by more than 7 to 1 at that scale.

Big concern #3: Alternative investment fees are way too high

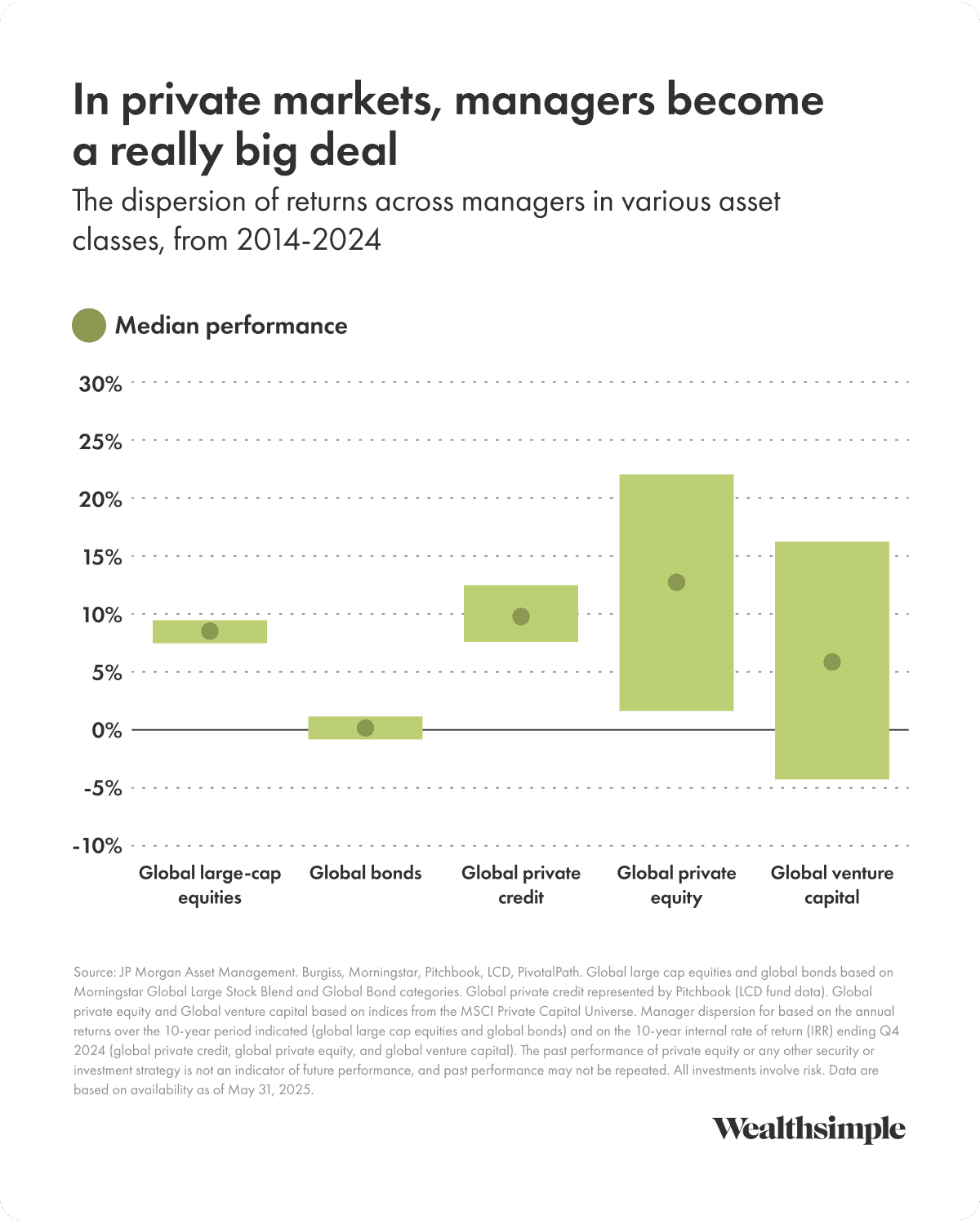

If you’ve read any of our investor newsletters over the last few years, you know we love to rail on fees. High fees can quietly erode an investor’s return over time. That’s why we believe in keeping costs low wherever possible. That’s especially true in public markets, where low-cost, passive index investing has long been a winning path.

But private markets operate under different conditions. There are no “passive” solutions available today. They’re more complex, with very little available information. Returns are much more widely dispersed, and top-tier managers have a better track record of staying at the top. (Check out the next chart to see just how big the difference can be.) They are better at identifying opportunities, structuring deals in ways that benefit their investors, driving operational improvements, and getting out of investments when it produces the most profit — and they’re able to demand higher fees because of it. If you don’t have a good manager, you often don’t have a good investment.

The other thing to consider is that alternative investments have historically outperformed public markets over the past two decades, even after you subtract the fees.

Big concern #4: Retail investors don’t get access to the same deals as the big guys

There’s an idea out there that individual investors in evergreen funds get whatever’s leftover after big institutions take their pick of potential opportunities — and that if things go south, it’s the individuals who will be left holding the bag. But well-run evergreen funds follow similar due diligence, governance, and investment standards as their institutional counterparts. Managers of these funds — who most often operate in both retail and institutional channels — have strong incentives not to accept second-tier opportunities for reputational reasons. (They also get paid more if their funds do well.)

Big concern #5: Alternatives are too risky

This misconception is primarily based on oversimplifications of how private equity and private credit work. With private equity, people often assume that investors profit simply by manipulating a company’s balance sheet, using tricks to squeeze out any money they can, and leaving investors with a faltering company they’ll be lucky to unload. Which, yes, would be risky. But good managers find opportunities to make long-term improvements that’ll make companies run better, creating actual value that makes them easier to sell for a profit when the time comes.

With private credit, a lot of investors think the loans made to companies are all equal. If the borrowing company runs into trouble, they think their investment is lost. But under a good manager, private credit loans are first in line to be paid back, which greatly reduces the odds of losing the investment and reduces risk.

At the end of the day, investing is about achieving outcomes that matter to you, and that’s going to be different for every investor. Alternative investments are simply one set of tools in the broader toolkit, offering the potential for strong returns and greater diversification. And to the extent that you have access to best-in-class managers, with demonstrated track records of strong performance, on time horizons that align with your needs, alternatives can play a valuable role in helping you achieve your goals.

Interested in alternatives?

Our private equity and private credit funds can help diversify your portfolio and boost returns.

Apply nowLegal

Have questions? Visit our Help Centre or submit a request to our Client Support team.

Private credit involves risks including, but not limited to, credit risk, liquidity risk, leverage risk and value fluctuation. See here for more information.

All information and commentary provided is for illustration purposes only and is not investment advice or recommendations. All investments involve risk. To get more info on our products, investment decisions, fee schedules, user testimonials, promos & more visit wsim.co/disclaimers.

The content of this message is confidential. If you have received it by mistake, please inform us by email reply and then delete the message. Do not copy, forward, or in any way reveal the contents of this message to anyone.

Managed accounts are offered by Wealthsimple Inc., a registered portfolio manager in each province and territory of Canada.

© 2025 Wealthsimple Technologies Inc.