Six questions you may have about your RRSP

The RRSP FAQ

February 7, 2024

During our December tax webinar, we opened up the floor to questions. And you all had a lot of questions. More than 200 people raised their digital hands, and while we did the best we could to get to everyone, 15 minutes was not nearly enough time.

That’s why we decided to dedicate this email to the topic that came up the most: RRSPs. The most important thing to know about them is that the 2023 contribution deadline is February 29. Otherwise, here are our best answers to a few of your biggest questions. (For the rest of your questions — on RRSPs, FHSAs, TFSAs, RRIFs, and other tax-protected accounts — click here.)

1. How much contribution room do I have? And do things like pension deductions, group plans, or dividends affect that room?

Every year, you build contribution room — either 18% of your income from the year before or the annual cap (2023’s is $30,780; 2024 will increase to $31,560), whichever is smaller. The CRA includes your RRSP limit every year in your Notice of Assessment. Any room you don’t take advantage of carries forward indefinitely, so even if you can’t save it all now, you can catch up later.

If your employer has a Group RRSP, any money you receive from it counts against your cap. It’s the same for Registered Pension Plans and Deferred Profit-Sharing Plans, although in those cases contributions count against your limit the year after they are made. Interest, capital gains, and dividends don’t affect contribution space at all.

2. What happens if you over-contribute to your RRSP?

It’s not the end of the world, but it will cost you. The CRA gives you a lifetime buffer of $2,000. Once you exceed it, you’ll pay a penalty of 1% of the excess amount each month. In case that doesn’t scare you straight, you’ll also have to fill out a T1-OVP form, which nobody wants to do.

3. Do RRSP funds have to be used for retirement?

RRSPs are a lot more flexible than people realize. You can take your money out at any time and for any reason. But unless that withdrawal is to purchase your first home (using the Home Buyers’ Plan) or go back to school (with the Lifelong Learning Plan), you will be taxed on it at your marginal tax rate at the time of withdrawal, like regular income.

4. As someone new to Canada, I have never filed taxes, which means I cannot start an RRSP. What is the best way for someone in my position to reduce my taxable income?

Although it won’t reduce your taxes this year, you could open a TFSA to allow your investments to start growing tax-free. Any resident of Canada who has a valid SIN and who is at least 18 years of age is eligible to open one. Once you do file taxes, you’ll know exactly how much RRSP contribution space you have — and you’ll be able to open and contribute to an RRSP at that point.

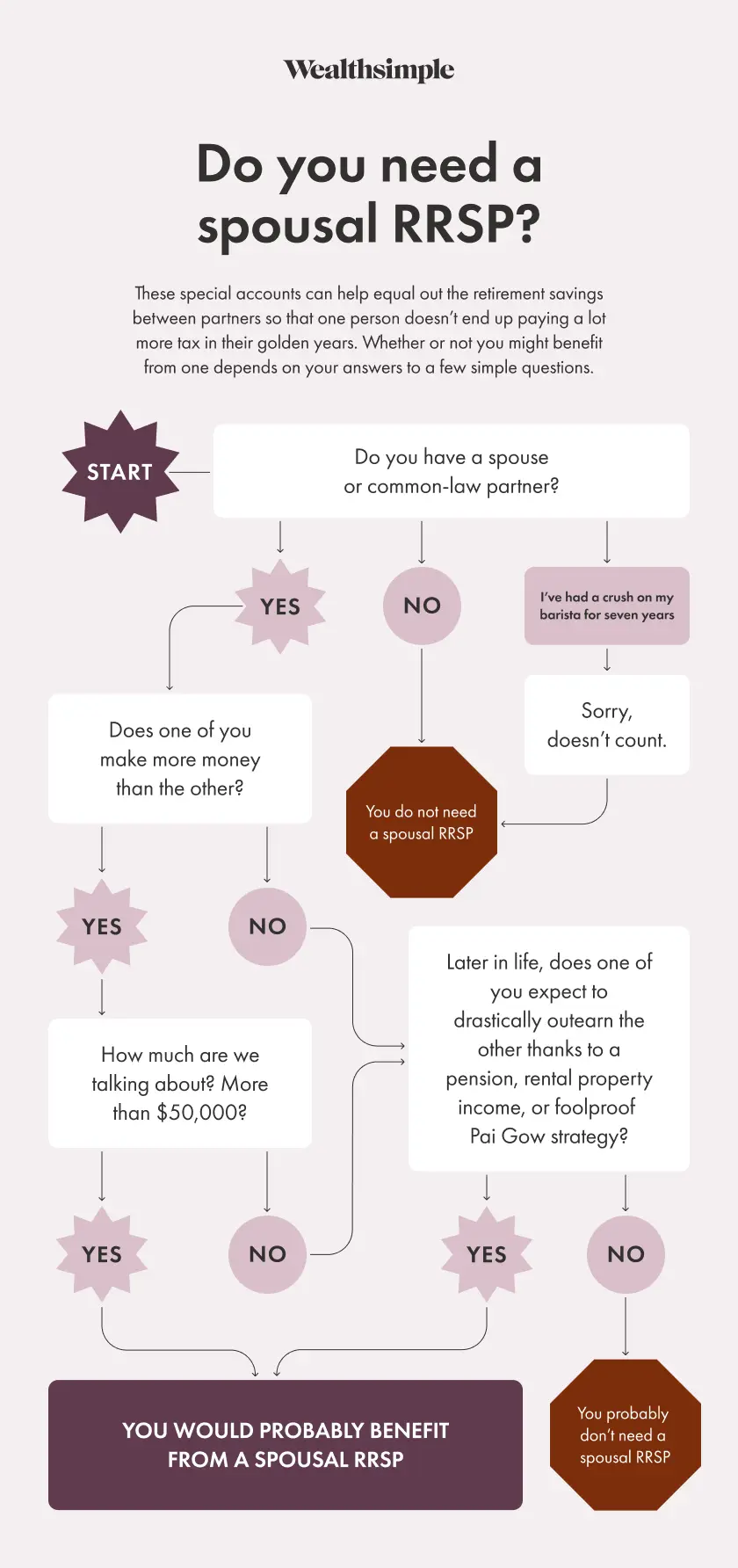

5. When should you use spousal RRSPs?

Spousal RRSPs are a special type of RRSP that can be helpful when one spouse has a meaningfully higher income than the other. That’s because, in a graduated tax system, it’s better for each person to have $40,000 of income than for one to have $65,000 and the other $15,000. With a spousal RRSP, couples can more evenly contribute to their accounts so that one person doesn’t have a substantially larger RRSP in retirement — and, therefore, end up in a higher tax bracket when they withdraw their money. The spousal RRSP is owned by the lower-income-earning spouse, contributed to by higher-income-earning spouse, and counted against the contributing spouse’s RRSP contribution room.

Not sure if a spousal RRSP is right for you? We made a flowchart to help.