Are tariffs and other unsettling news making you jittery?

How to handle market uncertainty

April 1, 2025

This year has already had plenty of attention-grabbing headlines: tariffs, geopolitics, tariffs, market uncertainty, tariffs. And now we have a new federal election coming, too. Nobody knows what the lasting effects will be on the economy, much less the world, but massive changes and uncertainty tend to lead investors to consider making drastic changes to their portfolios.

The subject has come up on multiple calls with clients lately. And our advisors’ response is often the same: look away, if you can. As dramatic as the news may get, the impact on many portfolios — especially well-diversified portfolios at risk levels that track with your goals — has been minimal. If things were to get worse, for investors with longer time horizons, even scary news tends to have little effect on your eventual retirement aspirations.

In fact, studies mostly show that downturns aren’t investors’ biggest enemy. It’s how they react to those downturns. Why might that be? Our brains just aren’t wired to process every small fluctuation calmly. It triggers a well-known phenomenon in finance called loss aversion, a sneaky bias that makes the possibility of losses feel way worse than the joy of potential gains.

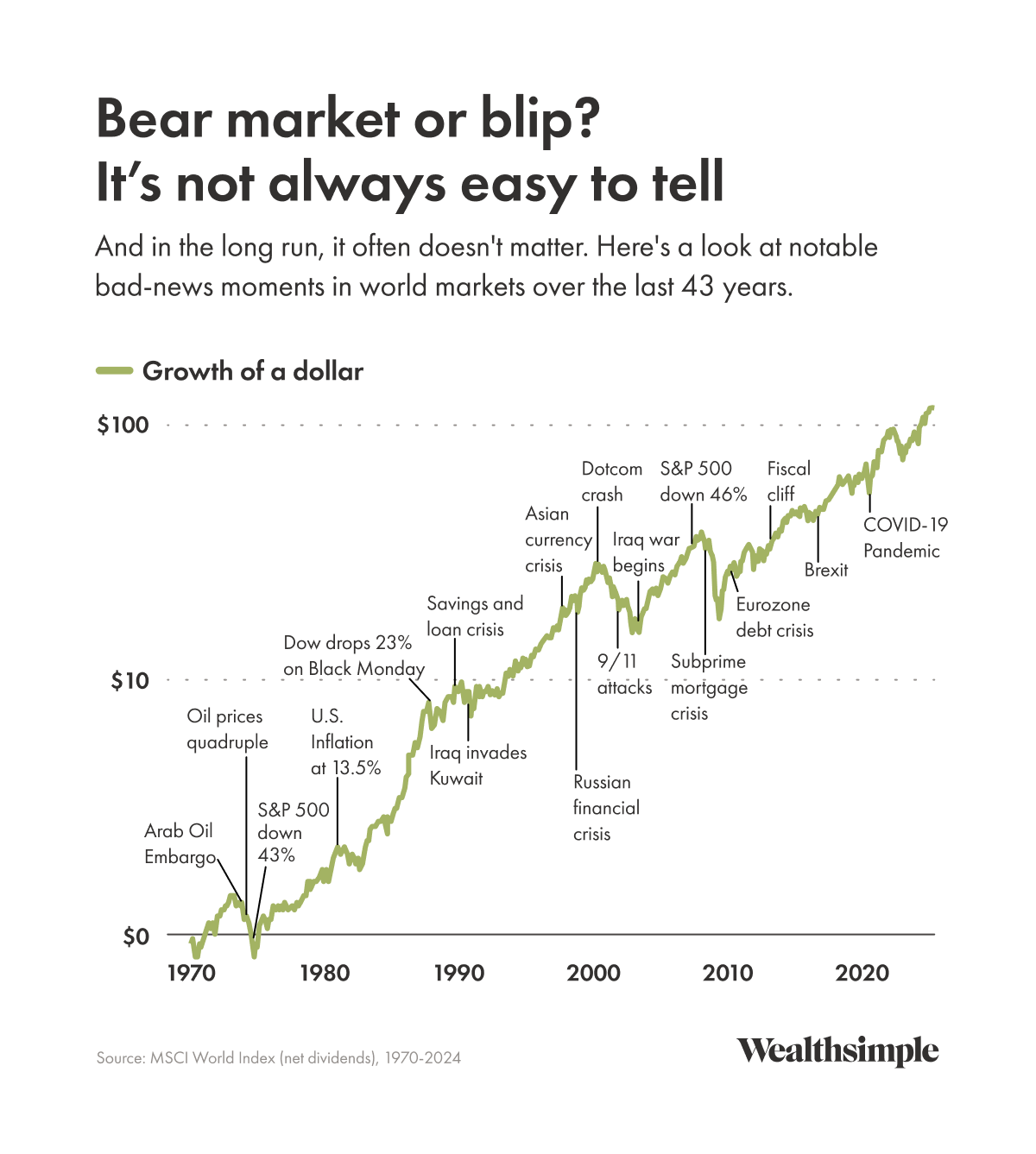

The reality is that uncertainty and market volatility are common. Since the 2008 financial crisis, it’s basically been one big bull market — but we’ve had 30 downturns like the one that kicked off earlier this year. Historically, a market drop of 5% has occurred roughly every year, with a drop of 10% or more happening about two out of every three years. Each one of those drops may have felt scary, but your portfolio probably doesn’t remember them at all.

How you can prepare for market uncertainty

We always talk about trying to tune out the noise around investing, and the same advice applies here. But how to do that is different for different investors.

The most important thing is to set up a plan. Then, stick to it. Which is hard, I know! That’s why we often recommend setting up recurring investments, which takes you and your emotions out of the equation by, say, having RRSP contributions withdrawn from every paycheque, or a certain amount of your savings invested in a particular group of assets each month.

We’ve also had clients benefit from something as simple as changing the timeframe on how their portfolio returns are presented from 1 month to all-time. The broader perspective can be reassuring. For other people, the trick is to avoid looking at their account balances completely, until well after the bad news has passed.

Of course every investor is different, and this stuff truly can be scary. So if, even after implementing these steps or wallpapering your washroom with the chart above, you find yourself in a dark and never-ending doomscroll, ask for help. A friend or financial advisor can often keep your fears at bay until better times — and better headlines — are back.